SMM, December 19:

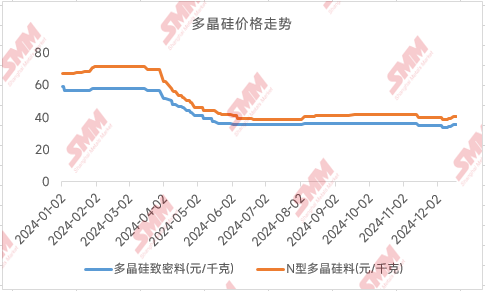

According to SMM data, the long-stagnant polysilicon prices have recently seen a recovery. Starting from December, polysilicon prices have risen for two consecutive weeks. At the end of November, polysilicon transaction prices were maintained at around 38 yuan/kg. As of now, some delivery prices have approached 40 yuan/kg. During the order signing period, several mainstream producers have collectively quoted 42 yuan/kg.

SMM understands that this price increase is mainly driven by mainstream enterprises actively standing firm on quotes. The convening of association meetings has led to effective progress in industry self-discipline, resulting in a certain recovery in market confidence. Polysilicon futures will officially launch on December 26, providing polysilicon producers with more options. Coupled with other factors such as price increases in downstream segments, polysilicon prices have risen.

Currently, polysilicon seller inventories remain at the level of 278,000 mt. Although supply and demand have become tightly balanced in December due to production cuts, considering that inventories have not shown a true supply shortage, the situation remains stable.

Regarding future trends, SMM understands that polysilicon producers exhibit strong sentiment to stand firm on quotes in this round of pricing. Currently, traceable materials and even some high-quality polysilicon are quoted at 44-45 yuan/kg. Combined with the potential for production increases in the silicon wafer segment, the probability of further increases in polysilicon order signing prices is high, with the market showing a high acceptance of the 42 yuan/kg price. However, it is worth noting that the polysilicon price increase still lacks fundamental support from supply and demand. In January and the subsequent months, module demand is expected to remain weak, and prices are likely to lack support during the traditional off-season of January-February.

》View the SMM PV Industry Chain Database

![[SMM PV News] AIKO ABC Modules Officially Delivered to Jingneng Kubuqi Desert Phase I 240MW Project](https://imgqn.smm.cn/usercenter/AuVub20251217171738.jpg)

![[SMM PV Flash] Pakistan | Hoymiles Deepens Local Cooperation, Ushering in a New PV+ESS Chapter in South Asia through Synergistic Efforts](https://imgqn.smm.cn/usercenter/LMmrH20251217171737.jpg)

![[SMM PV Express] Yingli's first batch of Panda high-efficiency modules arrived smoothly at the Yunnan Baoshan PV project site.](https://imgqn.smm.cn/usercenter/amiuR20251217171743.jpg)